")

")

Foreign market entry modes can differ significantly in degree of risk they present, the control and commitment of resources they require, and the return on investment they promise.

There are two major types of entry: equity and non-equity. The non-equity category includes export and contractual agreements. The equity category includes joint venture and setting up wholly owned subsidiaries.

A Slovak company can commence operations in India by incorporating a company under the Companies Act through Joint Ventures (JV) or a subsidiary (including a wholly owned subsidiary). Incorporating a private or public company or One Person Company (OPC) as a subsidiary in India involves paperwork for approvals and other formalities. In addition to the basic procedures, depending upon the sector and nature of business activities, companies may need to register with the relevant sector regulators.

For incorporation and registration, a set of applications have to be filed with Registrar of Companies (ROC). The Indian Chamber of Commerce and Culture offers a full company incorporation service which also includes handholding support after incorporation. For more information see below charts.

Choosing the right market entry strategy for India requires careful consideration of the needs, capacities and format of each particular business. Whether you choose to set up a subsidiary, a liaison office or a joint venture, there are several options available, each with different implications and advantages.

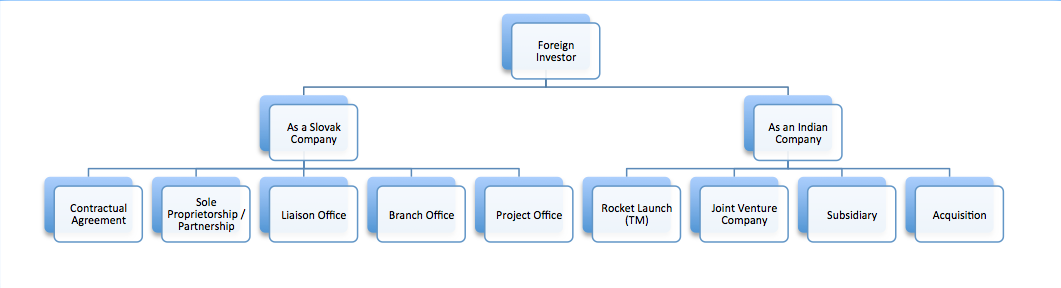

The following flowchart outlines the legal business structures you can set up in India, operating as either a Slovak company in the country or registered as an Indian company:

Market Entry Structures

As a Slovak company:

|

|

Description |

Advantages |

Disadvantages |

Other comments |

|---|---|---|---|---|

|

Contractual agreement |

• Simplest method of establishing a clear relationship between a Slovak company (SKCo) and an Indian partner (e.g. SKCo appoints Indian partner as a distributor in India). |

• No separate legal entity so setting up does not involve procedural formalities, which can be lengthy for separate entities such as a company. • Compared to other structures, requires less ongoing administration such as statutory filings. • Set-up costs will be the costs for negotiating and concluding contract. • Privacy of arrangements. |

• SKCo may be exposed to unlimited claims and liabilities in India due to its own actions and those of Indian partner. Ensure you seek Indian contractual advice. • Taxation is simpler but there are no tax advantages linked to a contractual arrangement. • Need to ensure no partnership formed. • Success in India is dependent upon a third party |

• Contractual documents need to be carefully drafted to minimise risks of SKCo having a permanent establishment in India and ensuring SKCo IP is protected. |

|

Sole proprietorship concern/ Partnership |

• Though a contractual relationship, substantively different from contractual relationships described above. Governed by Partnership Act 1932. |

• Control and privacy for business partners. • Simple to set up and no formal administrative burdens. • Potential to gain from business presence of Indian partner. |

• Practical difficulties for FDI, sectoral and banking restrictions for non-Indians. • No separate entity and unlimited joint and several liability risk between partners. |

• Many businesses/ individuals may already be doing business this way without formal recognition. |

|

Branch office |

• An extension of Slovak set up in India, which can undertake some but not all of the same activities as SKCo. The scope of its permitted activities will be determined by the permission that is granted by the Reserve Bank of India (RBI). |

• Can perform some revenue generating activities in India, unlike a liaison office (see below). • It is a separate legal entity for certain purposes. |

• SKCo may be exposed to unlimited claims and liabilities in India owing to branch office operations. • Restrictions on range of activities, which are subject to RBI approvals. • Formalities and legal set-up costs are involved. |

• Several airline and shipping companies have established Indian branch offices. • Tax structuring possible as branch office is taxed separately in India. The rate of tax is higher than the rates applicable to companies. |

|

Liaison office |

• Set up primarily to give an India face to SKCo and for marketing purposes. |

• Fewer ongoing formalities although there are set-up costs. • No separate legal entity but does provide a formal presence for SKCo in India. |

• Cannot trade or generate revenue in India. • SKCo may be exposed to claims and liabilities in India. |

• Must be funded by SKCo only • Minimum period of profitability and net worth requirement. |

|

Project office |

• Set up primarily if the SKCo has a secured contract from an Indian company to execute a project in India. |

• Prior RBI approval not required if certain conditions are fulfilled. • A project office is permitted to operate a bank account in India and may remit surplus revenue from the project to the SKCo. |

• The activities of a project office must be related to or incidental to the execution of the relevant project. |

• Project offices are generally preferred by companies engaged in one-time turnkey or installation projects. |

|

Rocket Launch(TM) |

• A stepping stone to Incorporation or a joint venture. Indian Chamber of Commmerce and Culture in Slovakia recruits, employs and manages a dedicated consultant that works on your behalf, and to a brief set by you. |

• No up-front investment costs. • Guaranteed control of your in-market spend. • Flexible budget to scale up your operation. • No need to source, secure and fit-out real estate. • Dedicated consultant on the ground quickly. |

|

• For more information on Rocket Launch(TM) contact This email address is being protected from spambots. You need JavaScript enabled to view it. |

As an Indian Company:

|

|

Description |

Advantages |

Disadvantages |

Other comments |

|---|---|---|---|---|

|

Joint venture (JV) company |

• SKCo and an Indian partner incorporate Indian company (JVCo) through which they carry on business. Can all use an LLP. |

• Separate legal entity and limited liability for SKCo. • SKCo benefits from Indian partner’s presence, business contacts and experience. • JVCo may raise further finance through new share issues or from lenders and pledge security using JVCo’s assets. |

• Set up can be time consuming and involves costs. • Negotiations with a JV partner and carrying out due diligence can be time-consuming. • Publicity requirements in relation to accounts and shareholdings as with any other limited company. |

• Various European companies enter India through JVs. • FDI is restricted in certain sectors and Indian shareholder requirement can be overcome by a JV can. • Can be tax advantageous. • Detailed due diligence and picking the right partner is key. |

|

Subsidiary |

• SKCo incorporates an Indian subsidiary (IndCo) to carry on business. |

• Unlike a JV company, SKCo 100% controls the strategic direction of IndCo. • SKCo’s liability in India will be limited. IndCo may raise further finance through new share issues or from lenders and pledge security using IndCo’s assets. |

• Setting up IndCo may delay the exploitation of immediate business opportunities. • Publicity and formalities as with other limited companies. |

• Only suitable where 100% FDI permitted, e.g. manufacturing and wholesale trading. |

|

Share acquisition of Indian company directly or indirectly |

• SKCo acquires a controlling stake in an Indian company (Target). |

• SKCo acquires all of shares of a Target, therefore acquiring all assets including any goodwill, reputation and licences. • Corporate structuring and tax efficiencies may be possible. |

• SKCo is responsible for any historic and existing obligations and liabilities of Target. • No Indian partner benefits with 100% acquisition. |

• Pre-acquisition due diligence required on Target. • Tax issues important. • Used particularly where there is existing consent, client base or asset, which would be expensive or difficult to transfer. |